Starting, running or reshaping a business later in life can be one of the most rewarding challenges we face.

With experience comes perspective, practical judgement and the ability to focus on what truly works.

This section of Ropho shares straightforward business insight drawn from real-world consulting across different industries.

You will find ideas on planning, leadership, financial awareness, marketing and sustainable growth.

Not theory for its own sake, but guidance designed to help you think clearly and move forward with confidence.

Whether you are launching something new, stabilising an existing business, or simply exploring your options, the aim is the same.

To build work that supports your lifestyle, reflects your values and remains purposeful in the years ahead.

Because business after sixty is not about proving anything.

It is about using experience wisely.

Read More – Busy All Week. Still Stuck? Try This Instead.

Weekly Series – An Overview of how to Plan and Run a business In Your Sixties

“Is it too late to start a Business at 64 years old?”

In recent years, the entrepreneurial landscape in the United Kingdom has witnessed a remarkable trend.

An increasing number of individuals aged sixty and above are starting or growing their own businesses.

Whether motivated by a desire for independence, a passion for a particular field, or the pursuit of financial security in later life.

Older entrepreneurs bring a wealth of experience, resilience, and unique perspectives to the world of business.

This guide presents comprehensive advice tailored to support those over sixty who are embarking on or considering a business journey in the UK.

Understanding Your Motivation and Vision

Before delving into the practicalities, it is essential to reflect on your motivations.

Are you looking for a new challenge, a supplementary income, or a way to share your expertise?

Clarifying your goals and vision will help you choose the right business model and set realistic expectations.

Create a personal mission statement and, if you wish, a vision board to visualise your aspirations for this new phase.

Assessing Your Skills and Experience

One of your greatest assets as an older entrepreneur is your accumulated knowledge and skill set.

Take stock of what you have learned throughout your career and life experiences.

Identify transferable skills, such as leadership, problem solving, and communication, as well as areas where you may need to upskill, for example, in digital marketing or social media.

Many local colleges and adult education centres offer courses tailored for mature learners.

Do not underestimate the soft skills you hopefully develope as you get older, patience, empathy, negotiation these are all skills that are invaluable in business.

Choosing the Right Business Model

The right business model will depend on your interests, lifestyle, and whether you are prepared to take a risk.

Some options are particularly well suited to those of us over sixties include:

Consultancy or Coaching: Leveraging your professional expertise to advise or mentor others.

Franchises: Purchasing a proven business model can reduce some of the risks and provide ongoing support.

Online Retail: Selling products via online platforms, which can be managed flexibly from home.

Creative Pursuits: Turning hobbies such as arts, crafts, writing, or gardening into income-generating ventures.

Property Management: Investing in or managing properties, either independently or through established agencies.

Investigate your chosen sector thoroughly. Attend local networking events, seek out relevant trade associations, and read up to date UK market research reports.

Legal and Financial Considerations

Registering Your Business

Decide whether you will operate as a sole trader, partnership, or limited company. Each structure has different implications for tax, liability, and paperwork. The UK government’s GOV.UK website offers clear step-by-step guides to registration.

Tax and Pensions

Understand the impact of running a business on your personal tax and pension situation. Income from your business may affect your tax bracket and, potentially, your entitlement to some state benefits. Consult a qualified accountant or financial adviser with experience in later-life finance.

Insurance

Ensure you have adequate insurance, public liability, professional indemnity, and, if you hire employees, employer’s liability. If you plan to work from home, check with your home insurer about any business-related exclusions.

Funding and Grants

Older entrepreneurs often self-fund their ventures, drawing on savings or pensions. However, there are grants and loans available specifically for start-ups and mature business owners.

Explore schemes such as the Start Up Loans programme, the Prince’s Trust Enterprise Programme (open to all ages), and local council initiatives. Crowdfunding and angel investment are also increasingly accessible avenues.

Embracing Technology

Technology is a significant enabler for modern business. From cloud accounting systems to social media marketing, digital skills can streamline operations, cut costs, and reach new markets.

If you feel less confident in this area, seek training from community digital hubs, online tutorials, or local Adult Learning Centres. Many libraries also offer free classes for older adults.

Building Your Network

Networking is invaluable for learning, sharing ideas, and finding support. Join local business groups, such as your local Chamber of Commerce or Federation of Small Businesses.

There are also online communities specifically for older entrepreneurs, offering forums, webinars, and mentoring schemes.

Don’t forget the value of informal networks—friends, former colleagues, and family may offer advice, contacts, or practical help.

Marketing Your Business

Effective marketing is crucial for growth. Develop a simple, clear brand identity and communicate it consistently across all platforms. The essentials include: A professional website—your digital business card for potential customers.

Social media presence—choose platforms that suit your target market (e.g., Facebook for local communities, LinkedIn for B2B).

Word-of-mouth referrals—encourage satisfied customers to recommend you.

Traditional methods—flyers, local press, and community boards still have impact, especially in smaller towns and among older demographics. (See my business plan templates and other business advice) free to subscribers.

If you are new to digital marketing, small business support groups and online guides can help you get started. Consider hiring a freelancer for tasks outside your skillset, such as website design or copywriting.

Wellbeing and Work-Life Balance

Running a business can be demanding.

Prioritise your health and wellbeing by setting clear boundaries, taking regular breaks, and seeking support when needed.

Build a routine that allows for social activities, volunteering, or family commitments.

Remember, financial success is just one measure, many older business owners value flexibility, purpose, and the joy of learning above all.

Common Challenges and How to Overcome Them

Age Stereotypes: Some may doubt your ability to innovate or adapt. Counter this by showcasing your achievements and willingness to learn.

Physical Demands: Choose a business model that fits your lifestyle and capabilities. Consider remote work or flexible hours.

Access to Finance: If traditional banks hesitate, explore alternative funding sources such as credit unions, peer-to-peer lending, or government-backed schemes.

Keeping Up with Trends: Commit to lifelong learning through courses, podcasts, and reading the business press.

Useful Resources

- GOV.UK – Business and self-employed: Official guidance and registration (gov.uk/set-up-business)

- Age UK: Information and support for older entrepreneurs (ageuk.org.uk)

- Federation of Small Businesses: Networking, advice, and support (fsb.org.uk)

- Start Up Loans: Government-backed loans (startuploans.co.uk)

- Local Enterprise Partnerships: Regional business advice and funding (lepnetwork.net)

- Small Business Saturday UK: Campaign to support small businesses (smallbusinesssaturdayuk.com)

Conclusion

Launching or growing a business after sixty in the UK is not only possible, it can be immensely rewarding.

With a clear vision, the right support, and a willingness to embrace new opportunities, older entrepreneurs can thrive.

Your experience is your advantage, use it to create a business that reflects your values, fits your lifestyle, and brings value to your community.

Remember, the adventure of enterprise is open to all ages, the best time to start is now.

The Over-60s Business Planning Checklist

A practical pre-planning guide for starting, restructuring, or stabilising a business later in life

How to Use This Checklist

This checklist is designed to help you think clearly and realistically before writing a full business plan or committing time and money to a new venture.

You don’t need to answer everything perfectly. The aim is clarity, not complexity.

- Personal Readiness

☐ Why do I want to run a business at this stage of my life?

☐ What do I want this business to give me? (income, purpose, flexibility, security)

☐ How many hours per week am I realistically willing to work?

☐ What level of stress am I prepared to tolerate?

☐ Do I want growth, or stability and control?

- Experience & Skills Inventory

☐ What skills have I built over my working life?

☐ What problems can I genuinely solve for customers?

☐ What experience do people already trust me for?

☐ Could my experience be offered as a service, consultancy, or specialist trade?

- Business Model Clarity

☐ Is this a new business, an existing business, or a restructured one?

☐ Will I sell to businesses (B2B), consumers (B2C), or both?

☐ Do I want hands-on work, advisory work, or a mix?

☐ Can this business operate without me being present every day?

- Market Reality Check

☐ Who exactly is my ideal customer?

☐ What problem am I solving for them?

☐ How are they currently solving that problem?

☐ Why would they choose me instead?

☐ Do I understand my competitors and pricing?

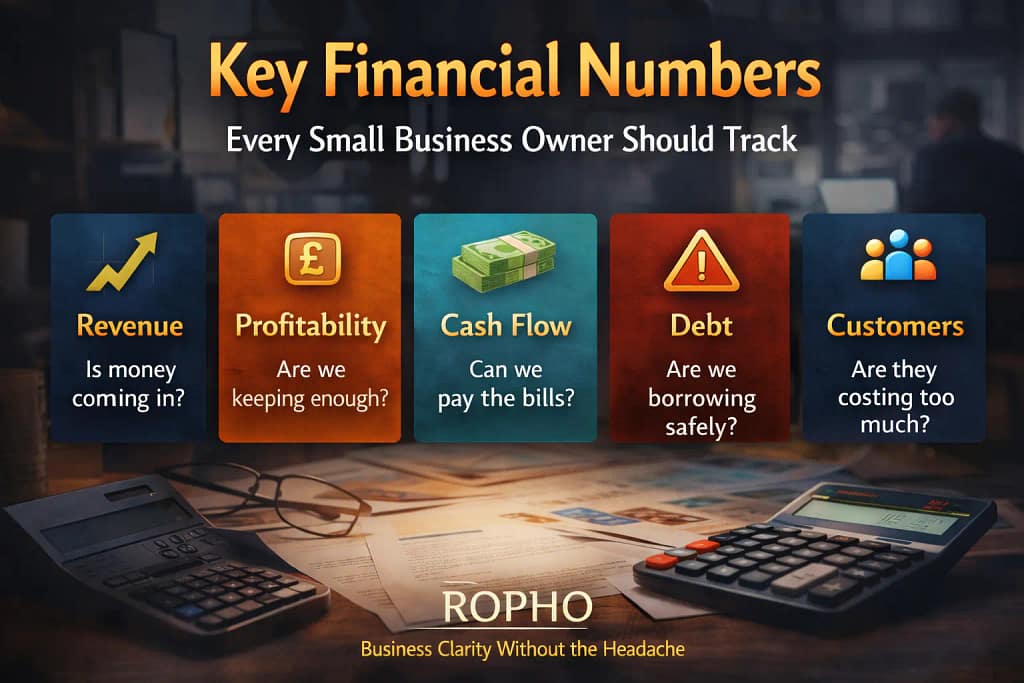

- Financial Awareness

☐ How much income do I realistically need from this business?

☐ How long can I operate before the business must pay me?

☐ What are my fixed monthly costs?

☐ What are my biggest financial risks?

☐ Do I understand my break-even point?

- Risk & Regulation

☐ What licences, qualifications, or permits are required?

☐ What health and safety responsibilities apply?

☐ Are there insurance requirements I must meet?

☐ What are the consequences if something goes wrong?

- Lifestyle Fit

☐ Does this business fit around my personal life?

☐ Can it be slowed down or scaled back if needed?

☐ Does it allow holidays or downtime?

☐ Will this business improve or reduce my quality of life?

- Exit & Future Thinking

☐ Do I want to sell this business one day?

☐ Could it be handed over to family or staff?

☐ Can it operate without my direct involvement?

☐ What does success look like in 3–5 years?

Final Thought

If you can answer most of these questions clearly, you are in a strong position to create a practical, realistic business plan.

This checklist forms the foundation of a more detailed planning process, which is covered in full in The Practical Business Plan Guide.

PDF available free to subscribers